May 2024

Supporting employee health in a cost‑conscious climate

Balancing employee health care coverage with affordability is an ongoing challenge for employers. Getting this right is critical—and the stakes are high. Health care benefits play a key role in attracting and retaining talent. They’re also an essential component in whole-body employee wellness, with physical, financial and mental health all interconnected. In addition, employers recognize that workplace wellness is linked to workplace productivity. For all these reasons, let’s take a look at strategies employers are implementing to help support employee health in a cost-conscious climate.

HDHP + HSA: Benefits for employees and your bottom line

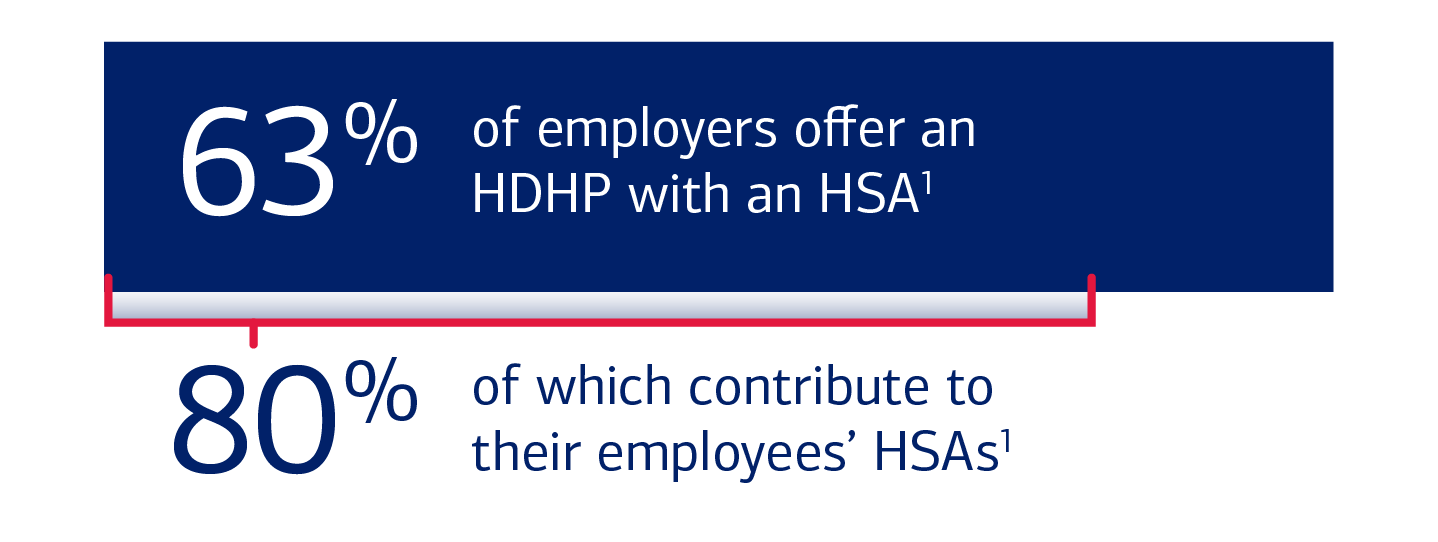

High-deductible health plans (HDHPs) typically offer lower monthly premiums than traditional health insurance plans, thereby offering the opportunity to save your company and your employees money. HDHPs may appeal especially to younger or healthier employees who don’t require frequent medical visits or supplies. These employees may opt to pay out of pocket as necessary vs. paying monthly for more expensive coverage they may not need.

Another attractive feature of an HDHP is the ability to pair it with a Health Savings Account (HSA) to help employees pay for out-of-pocket health care expenses and prepare for unexpected and future expenses, including in retirement. HSAs can help employees’ health care dollars go further through potential tax savings—federal income tax-free contributions, tax-free earnings and tax-free withdrawals2—that can add up and give employees more buying power for their health care needs.

|

|

Did you know?Your organization can also realize savings through tax-deductible contributions to employees’ HSAs and lower FICA taxes when employees contribute to their HSA through payroll deductions. |

Long-term benefits of an HSA

What makes an HSA stand apart from other health accounts is that there is no “use it or lose it rule,”3 and any unspent dollars remain in the account year after year. This gives employees the opportunity to build their balance over time and create a health care nest egg. Having access to these funds can help reduce employees’ stress as unexpected medical expenses arise, and can also help employees feel better prepared in the face of rising health care costs.

A 65-year-old couple may need as much as $351,000 to cover health care costs in retirement.4

An often-overlooked feature of an HSA is the ability for account holders to invest a portion of their balance in mutual funds for tax-free growth. A surprising number of employees, as well as employers, don’t realize that their HSA dollars could be working harder for their future by taking advantage of the HSA’s investment feature.1,5 More education may be needed to increase understanding of HSA investing, so these accounts can be used to their full potential as part of a long-term savings strategy.

Putting employees in charge of their health

Corporate wellness programs can encourage and reward healthy behaviors. They can include a range of initiatives and benefits, from a workplace fitness challenge to a Lifestyle Spending Account (LSA)—which is an employer-funded account that employees can use to help pay for a designated list of wellness expenses. Such efforts can provide a return on investment for employers, such as higher morale, lower absenteeism, increased engagement and productivity, and improved recruitment and retention.

To support employees in taking charge of their health, employees need to be aware of the opportunities available to them. While the majority of employers feel responsible for employees’ understanding of heath care options and costs, most plan sponsors communicate this information only once or twice a year.1 Empowering employees with access to yearlong educational programs and resources can help them become better health care consumers—helping keep your company’s health care costs in check and assisting employees in navigating their own health care needs and budgets.

Key takeaways

- Consider offering an HSA with an HDHP to help employees pay for qualified medical expenses now, with the potential to save for health care costs in retirement.

- Encourage employees to take advantage of our Health & Benefit Accounts Learn Center and educational webinars.

- Download resources you can use in your own communication channels to help educate employees on HSAs and tips to make the most of them.

Investing involves risks. There is always the potential of losing money when you invest in securities.

1 Bank of America 2024 Workplace Benefits Report.

2 Potential Tax Advantages: You can receive federal income tax-free distributions from your HSA to pay or be reimbursed for qualified medical expenses you incur after you establish the HSA. Any interest or earnings on the assets in the account are federal income tax-free. If you receive distributions for other reasons, the amount you withdraw will be subject to income tax and may be subject to an additional 20% tax, unless an exception applies. You may be able to claim a tax deduction for contributions you, or someone other than your employer, make to your HSA directly (not through payroll deductions). In addition, HSA contributions may reduce your state income taxes in certain states. Certain limits may apply to employees who are considered highly compensated employees. Bank of America recommends you contact qualified tax or legal counsel before establishing an HSA.

3 “Never lose it” refers to account portability and annual rollover of accumulated assets; it does not imply you cannot lose money. The investment portion of the HSA account is not FDIC insured, not bank guaranteed and may lose value.

4 Employee Benefit Research Institute (EBRI), Issue Brief, no. 599, January 18, 2024.

5 Mutual Fund investment offerings for the Bank of America HSA are provided by Merrill Lynch, Pierce, Fenner & Smith Incorporated (“MLPF&S”), a registered broker-dealer, registered investment adviser, Member SIPC, and a wholly owned subsidiary of Bank of America Corporation. Investments in mutual funds are held in an omnibus account at MLPF&S in the name of Bank of America, N.A., for the benefit of all HSA account owners. Recommendations as to HSA investment menu options are provided to Bank of America, N.A. by the Chief Investment Office (“CIO”), Global Wealth & Investment Management (“GWIM”), a division of BofA Corp. The CIO, which provides investment strategies, due diligence, portfolio construction guidance and wealth management solutions for GWIM clients, is part of the Investment Solutions Group (ISG) of GWIM.